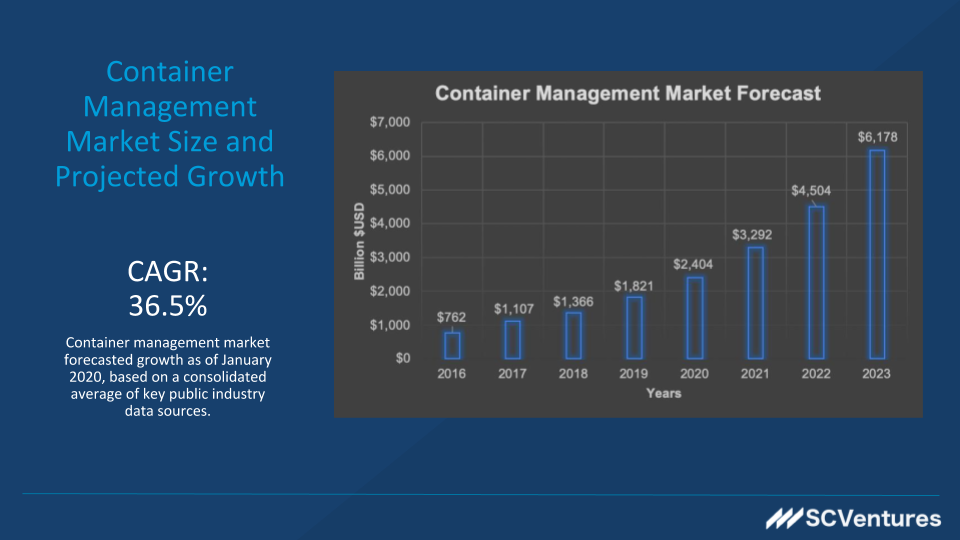

Definitive Market Guide Series – Container Management 2020

In this blog, I wanted to take a quick look at what is ahead for 2020 in the Kubernetes and associated markets as part of our “Definitive Market Guide” series for 2020. Legacy container management platforms such as Swarm, Mesosphere, and even Amazon ECS are seeing a slowdown in adoption.

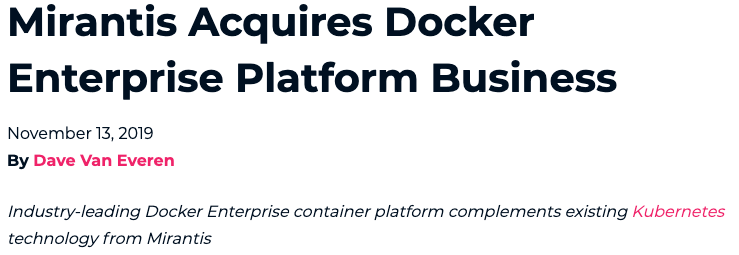

Kubernetes and cloud-native technology markets are continuing to evolve at a rapid pace. With 2019 seeing further consolidation with the container orchestration segment as Docker becomes a part of Mirantis and Mesosphere trying to reposition itself as a “Day-Two” company (D2IQ), distancing itself from their legacy products while ramping up to adopt Kubernetes.

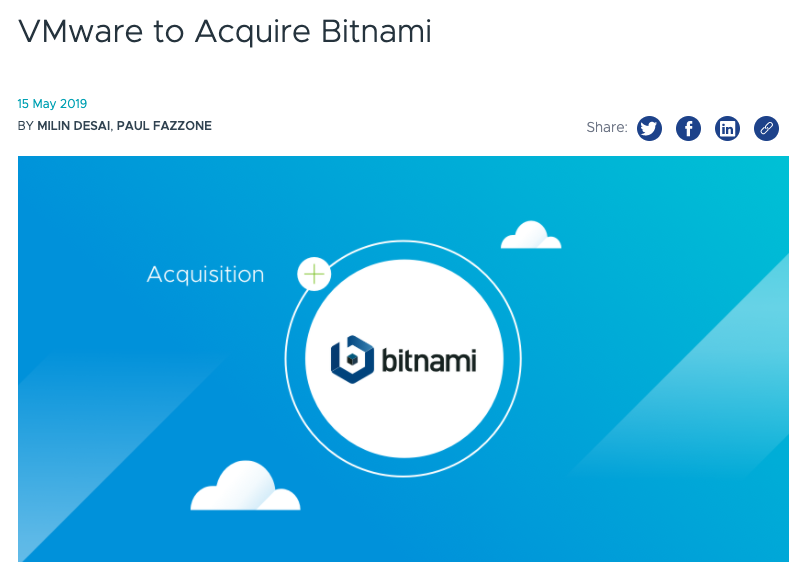

VMware also stepping up to the plate with the $550M acquisition of Heptio which was closed in Q4 2019. This building on their acquisition spree as they bring Pivotal into the fold and work to structure their new Tanzu architecture for the next stage of their efforts to co-opt Kubernetes and defend their virtual machine market dominance. Additionally, VMware picked up Bitnami an application repository and packager of applications for easy deployment on VM or Kubernetes environments via Helm charts.

2019 Also saw the close of the $34B IBM acquisition of Red Hat, two other players in the Kubernetes markets, with IBMs Kubernetes Cloud service and Red Hat’s Openshift platform, which the later is leading the market adoption for commercial Kubernetes distributions. With competing versions from both companies, customers will have a challenge in deciding their go-forward path.

Source: SCVentures – Definitive Market Guide 2020 – Container Management

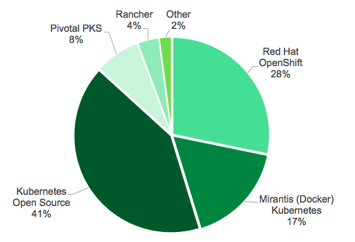

Still, with all the acquisitions, and investments by market elephants more than 41% of users are still using the pure open source versions of Kubernetes. The ecosystem showed healthy growth demonstrated at the latest KubeCon conference, in San Diego, hosted by the Linux Foundation’s Cloud Native Compute Foundation (CNCF.io) where more than 197 technology vendors participated and saw their largest number of attendees to date.

In the Definitive Guide for 2020, we also took a look at the vendor’s shares of the market today and how they expected to grow through 2020. In addition, how they are benchmarking against one-another and the pure open-source alternative.

With all this consolidation in 2019, what does 2020 hold ?

- With an overcapitalized market, expect to see more consolidation in the core orchestration services.

- Today there are few independent providers of core orchestration services. Rancher.io being one amongst others including a combination of SaaS-delivered and on-premise solutions from D2IQ, Kublr, Platform9, and a host of other start-ups which will find growth challenges.

- There remain key vendors without a container play, but not for long.

- While elephants like Amazon, IBM/Red Hat, and VMware have made committed investments (overinvestments), the second tier and a few first-tier have yet to make a move. Among these are Canonical, Microsoft, and SUSE.

- Last year’s acquisitions will continue to create confusion for customers.

- As each party wrestles with pulling all the pieces together in a way that customers can consume in a reasonable fashion, the door will be open for a few players to make progress against the Elephants.

We will continue to track the market to check back for updates. If you are interested in finding out more about our “2020 Definitive Market Guide for Container Management” or get a copy for yourself, simply follow this link.

Author: Scott Clinton

Scott has 20 years of industry executive leadership experience leading Developer, Software-defined infrastructure, Big Data, Hadoop, Security and Hybrid-cloud product portfolios for some of the industry’s leading global technology providers including EMC, Hortonworks/Cloudera, MobileIron, Red Hat, Qualys, VMWare, and Sun. Educated in Silicon Valley, Scott holds Bachelors of Computer Systems Design and International Business degrees.